Key To Landing The Lowest Mortage Rate

Buying a home is a huge decision as well as a financial commitment. When getting home, shopping for the lowest mortgage rates is a crucial strategy that can save you thousands of dollars over the loan. Spotting the right mortgage can be a difficult process. We will take you through a series of steps that will come in advantageous while finding the right mortgage.

Look For Options & Find The Right Bank

It might appear as obvious advice to shop around for the best interest rate you can get. But Chicago mortgage rates show that 81% of borrowers applied to just one lender, while 51% considered only one. A little time used on shopping around can help you get a much better rate. Seemingly small variances in interest rates can make a big difference in the long run, as mortgages involve high balances and long payment periods.

Check with your bank(s) first, but check with other banks too, and with credit unions, which often sport lower interest rates. You might also consult a mortgage broker. Home equity loans in Chicago and many places often offer a wide range of loans and can be helpful if you have an underwhelming credit record.

A Good Credit Score & Lower DTI

One of the powerful ways to get low-interest rates is to have a leading credit score. Lenders need to know that you're a good credit bet, so they place a lot of emphasis on it when they decide what interest rate to offer you. If your score isn't very promising, it can be worth spending some time adding it up along with your rates. There are three key ways to boost your score, such as - fixing errors in your credit record, paying bills on time, and diminishing your overall debt load.

|

| Home equity loans chicago |

A low debt-to-income (DTI) ratio shows a good balance between debt and income and a high DTI can indicate that an individual has too much debt for the amount of income he or she has. Buyers who have lower DTIs are more inclined to successfully managing their monthly debt payments, so lenders prefer to see these low numbers. In general, 43% is the highest DTI a borrower can have and still get suited for a mortgage.

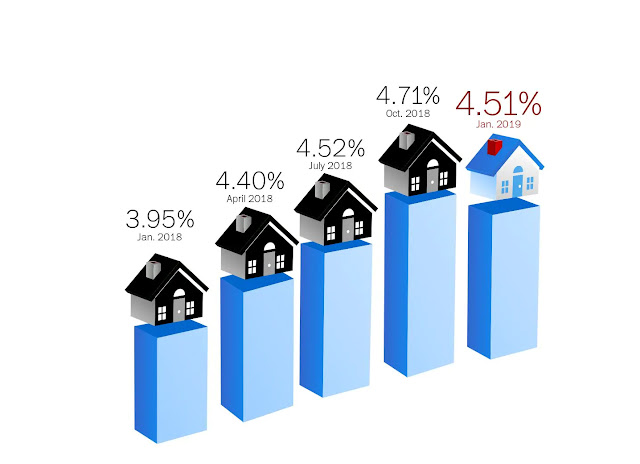

Lock in Low rates

Ultimately, be careful when deciding what type of mortgage to get. One with a lower interest rate may seem good but won't necessarily serve you best. When it comes to 15-year loans or 30-year loans, you'll be offered a lower rate for the shorter term. That can make a 15-year loan worth it, as you'll clear off your loan faster and you'll pay far less in interest, too. However 15-year loans have significantly larger monthly payments requiring you to spend more and pay over a long period.

Comments

Post a Comment